Finance Weekly Updates

Spirits Rise with Hedge Fund Gains

Hedge Fund managers have been in a good mood lately as world markets seem to head upwards, shaking off the unpleasant memories that hopefully is all that is left of 2008,one of the worst years in financial history.

The month of July alone saw the Eurekahedge Hedge Fund Index climb an additional 2.1 percent, adding another month to the five month growth streak of 2009.

To date the Index has improved an impressive 12 percent, with hopes for the rest of the year high.

Another index, the MSCI World Index soared 8.4 percent just in July bringing its year-to-date upward climb to 14%.

This extraordinary improvement relied mostly on the success of the fund managers of the Asian and emerging markets sectors.

“The month’s returns were achieved on the back of strong rallies across underlying equity markets despite a rough start to the month,” Eurekahedge wrote in its report.

This is good news to the hears of fund managers all over the world such as John Paulson, Eric Sprott of Sprott Hedge Fund

PIPE Investment Not a Pipe Dream For GM

As the financial world continues to feel the reverberations of one of the most daring, controversial and largest bailouts of a publicly traded company by the U.S. government in history, that is the General Motors decline into bankruptcy and the U.S. government’s bailout, Corey Ribotsky believes he is seeing just another PIPE investment, albeit on a grander scale.

In an opinion piece which appeared in HedgeWorld News, the managing partner and head portfolio manager of the NIR Group of Roslyn, New York, Corey Ribotsky, described the many ways in which the recent U.S. government bailout of General Motors Corporation resembles a PIPE deal which Ribotsky’s investment firm has been dealing with for years.

PIPE is an abbreviation for private investment in public equity, and according to Ribotsky’s take on the bailout, the U.S. government is investing in the publicly held equity of General Motors, or what’s left of it.

Investigators Warn: Stess Tests Not Enough

The Oversight Panel which is supervising the U.S. government bailout of banks to the tune of $700 billion issued a report Tuesday, June 9th, stating that the Federal Reserve used “conservative and reasonable” methods for the assessment of the well-being of the country’s largest banks.

However the panel also said that the Fed’s most pessimistic scenario was not far reaching enough. One example is that the “stress tests” which were conducted by the Federal Reserve bases their conclusions on 2009 unemployment figures which averaged 8.9%. This year unemployment actually reached 9.4% in the month of May.

“While no one should gainsay the potentially positive results of the tests, it would be equally unwise to think that those results reflect a diagnosis of all of the potential weaknesses or create a necessarily sufficient buffer against future reverses for the banking system,” warned the panel in their report.

Do Investors Get Unbiased Research From Wall Street?

Appearing before a United States’ House of Representatives’ subcommittee hearing to discuss “Analyzing the Analysts: Are Investors Getting Unbiased Research from Wall Street?” Gregg Hymowitz, a founder and principal of EnTrust Capital Inc. offered his opinion as testimony. This thought provoking testimony can be viewed in full by following the link.

Shareholders Arise: Take More Responsibilty for Banks’ Policies

Shareholders seem to be taking their rights more seriously as banks observe larger turnouts at their annual shareholder meetings. According to an article in the Wall Street Journal (which can be seen in full here) it has been observed by the proxy voting agency Manifest for Financial News that the average proportion of shares which were represented and the annual meetings of Europe’s twelve largest banks went up to 52% this year from 46% last year. This increase in attendance is seen as a response to the financial crisis which is perceived to be largely the fault of risky practices and other management decisions made by banks without the direct involvement of the majority of shareholders.

According to David Ellis, the corporate governance manager of proxy voting consultancy Pirc,

“The increase in turnout is not surprising given the issues faced by the banking industry over the last year and is an indication that shareholders are taking their rights as owners seriously and willing to keep management in check.”

“The figures are also a reaction to the crisis. The next step is for shareholders to get proactive and engage with companies to make sure it does not happen again.”

Turbulent Times

The past several months have been a roller coaster of ups and downs for the major market indicators. These markets are reflecting great uncertainty and the caution practiced by investors as the U.S. and international economic scene continues to show signs of trauma.

The Unique Advantage of Hedging with the NIR Group

As investors continue to feel the stress of bear markets, sluggish growth and financial uncertainty, many are looking for new ways and innovative strategies to make their dollars work harder for them.

One choice many investors have been exploring recently is investing in hedge funds. These specialized investment vehicles reduce the risk of market fluctuations on stock value while carefully choosing investments in companies with strong growth potential. This creates a fund which is less susceptible to the general market fluctuations and more likely to increase in real stock value.

There are many firms which specialize in hedge fund investment. One of these is the well-known NIR Group, headquartered in Roslyn, New York and headed up by Corey Ribotsky, head portfolio manager. The NIR Group has an additional unique feature, and that is the principals are not just managers of the funds, but are investment partners right along with their clients. This means that clients and managers always share the risks and are never subject to conflict of interest. This is a distinct advantage to investors and makes the NIR Group an excellent choice for investing at a time of economic uncertainty.

Investor and Money Manager Should Ride the Wave Together

In today’s investment world of bear markets and bankruptcy it is no surprise that investors are proceeding with utmost caution and reassessing their entire investment strategy. One area of investing that is perhaps taken for granted but shouldn’t be is the relationship between the money manager and the investor.

In today’s investment world of bear markets and bankruptcy it is no surprise that investors are proceeding with utmost caution and reassessing their entire investment strategy. One area of investing that is perhaps taken for granted but shouldn’t be is the relationship between the money manager and the investor.

Taking a deeper look we can see that there can be an inherent, if unseen, conflict of interest between the investor and the money manager whom he has hired to work for the best interests of the investor. Unless the money manager is equally invested with the people he is working for, there may be times when what is good for the money manager might not be equally good for the investor.

Harry Rady, CEO of Rady Asset Management located in San Diego, California has written an in depth article on this crucial subject. Rady is one of the more sought-after analysts of the economy today, frequently interviewed on CNBC’s “Closing Bell”, Fox Business News and other influential financial news programs. He also writes extensively on financial issues.

We recommend taking his opinion into account when about to embark on any new investment or financial decision.

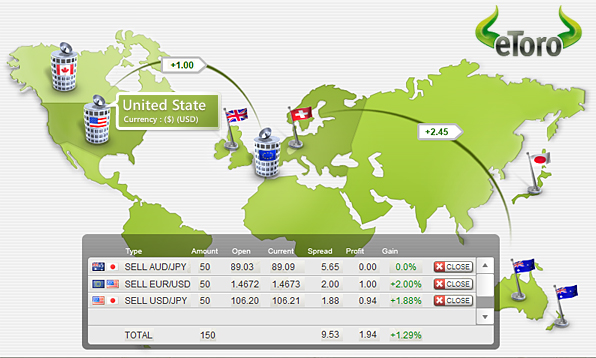

eToro’s Forex Trading Platform Secures $6.3M

Reprinted from http://www.vccafe.com

Israel-based eToro has secured $6.3 million in Series B financing from BRM Group, Cubit Investments and other unnamed investors. eToro offers an online financial trading platform that helps less experienced traders to easily conduct foreign exchange trades via a simple user interface. eToro’s interface provides six different “trading arenas” for traders ranging from beginners to experienced traders.

No matter if the economy is booming or crashing, traders thrive in volatile markets and eToro is enjoying the effects. Since September the company has doubled its staff, adding several thousand new users a month. Most recently, eToro added long term Commodities Trading.

According to CEO and Co-Founder Jonathon Assia:

“Our vision of becoming the online destination and trading platform for everyday people has taken a quantum leap forward with our new platform. With more long term investors turning to forex as financial markets around the world continue to struggle, eToro has developed the platform with tools and parameters for the more conservative forex investor on the go.”

Down we go again: Faint hope vanishes on Wall St.

NEW YORK — So you thought Wall Street might be out of the woods? Think again.

A surge of optimism that started a market rally late last year, mercifully quieting the stock market’s stomach-churning volatility, has vanished as economic recovery recedes further onto the horizon.

On Wednesday, stocks took a dive reminiscent of the terrifying jumps and drops of last fall, with the Dow Jones industrials falling more than 300 points before closing down 248.

It was the Dow’s biggest point drop since Dec. 1 and the first string of six straight down days since early October. The Dow is still 9 percent higher than its November low, but the bumpy decline feels all too familiar.

“It’s a good instinct to start a New Year off with optimism,” said Art Hogan, chief market analyst at Jefferies & Co. in Boston. “But unfortunately that tends to fade in the harsh light of reality.”

So what happened?

Holiday sales turned out to have been worse than expected, the jobless rate exceeds 7 percent for the first time in 16 years, the global economy is eroding faster and corporations from Alcoa to Intel to Wal-Mart have disappointed investors.

Apple was the latest company out with bad news Wednesday, with CEO Steve Jobs saying he is taking a medical leave of absence.

“Right now we just don’t have any evidence to show that that free fall is over,” said Robert Dye, senior economist at PNC Financial Services Group in Pittsburgh.

For a time, it seemed like the worst might be over for stocks. After hitting a trough on Nov. 20, the major stock averages all rose by more than 20 percent within six weeks – the kind of rally that usually takes years.

The rally was driven in part by hopes for Washington’s aggressive fiscal policies and the upcoming change in the White House. But lately bears rule Wall Street again as one corporate report after another spreads gloom.

Like others, Dye thinks the market could fall back toward the low point of November. That was when the Standard & Poor’s 500 index reached its lowest close in 11 years, at 752, and the Dow reached its lowest in more than five years, at 7,552.

On Wednesday, the S&P closed at 843, the Dow at almost exactly 8,200.

Stock market recoveries usually precede economic recoveries by about six months. Translation: Investors don’t expect the economy to turn around before the second half of this year.

“Wall Street wants instant gratification, but economic cycles take years and an economic cycle like this is going to be deeper, longer and uglier than any one we’ve ever faced,” said Harry Rady, chief executive and portfolio manager for Rady Asset Management in San Diego.

Sam Stovall, chief investment strategist at S&P, puts it another way: Investors have put on their 3-D glasses, trying to figure out “the depth, the duration and the diffusion of this global economic slowdown.”

And not having much luck.

For now, Hogan says stocks may trade in a much narrower range than they did during the white-knuckle days of October and November, when the Dow routinely rose or fell by 500 points or more in a day.

That range is perhaps 8,000 to 9,000 for the Dow, and 825 to 910 for the S&P, Hogan says. But more bleak news from corporations or Washington could still steer it lower.

For those looking for hopeful signs, consider these:

– Only once since World War II have stocks bounced back 20 percent in a bear market without signaling the start of a new bull market, according to Stovall. That lends hope the surge could resume in the not-too-distant future.

– A huge amount of money that was pulled out of stocks in last year’s big sell-off remains on the sidelines and should re-energize the market at some point when investors see more encouraging signs, according to Liz Ann Sonders, chief investment strategist for San Francisco-based brokerage Charles Schwab Corp. At year’s end $8.85 trillion sat in cash, money markets and savings accounts, an all-time high, she noted.

Other experts urge calm and suggest putting the recent slide in perspective.

Robert Doll, global chief investment officer for the investment firm BlackRock, says the market’s latest swing down is normal and was to be expected after a 20 percent rise and some bad data.

“We’re going to get more bad data and we should expect some more selling squalls,” he said.

Just keep those rose-colored glasses in your drawer for a while.

Dye said stocks could fall again if Washington isn’t quick to come up with planned spending to boost the economy after President-elect Barack Obama takes office next week.

There is an expectation that we’re going to have an $800 billion package in place very quickly, he said. “If that doesn’t happen in a timely fashion that would be another negative for the markets.”

On Recessions and Depressions

What is the difference between a depression and a recession, and which are we experiencing now? Until the Great Depression, and for some time after, any downturn in economic activity was known as a depression. But in the late 20th century, economists and politicians were reluctant to alarm the public by using that loaded term, and so they coined the alternative, “recession” to denote a relatively minor economic downturn. Some have attempted to give formal definitions, based on the extent of shrinkage or the duration of the negative period. But the best definition remains the somewhat humorous one: “A recession is when other people lose their jobs. A depression is when you lose yours.” To this we may add, for the current recession: “A recession is when other people lose their homes, a recession is when you lose yours.”

The Year of the Flat Screen

Even with an atmosphere of restraint and a renewed commitment to fiscal responsibility, this may be the year when more Americans than ever get flat-screen TVs and computer monitors. It looks at though manufacturers have prepared too many for the holiday season, and will be forced to sell at rock-bottom prices. News of a federal investigation into price-fixing schemes between manufacturers also portends an imminent downturn in prices. We are already witnessing heavily reduced pricing in the context of holiday sales, below the traditional $10/inch barrier, and consumers are unlikely to accept a return to old prices once they have experienced the new lows.

British Real-Estate Crisis Looms

If you’ve been to the UK in the last couple years, you know how expensive land is there. The country is small, populous and developed, all factors that contribute to legitimate rise in land cost. But lately prices seem to have climbed beyond reasonable levels. Analysts have observed that there is not currently enough wealth in all of England to cover the mortgage costs held by the citizenry. This includes bank assets! Were homeowners to experience a “call”, there would be a huge shortfall and many would lose their homes, to banks who would then be unable to sell them for anywhere near their supposed value. The banks, in turn, would default on their obligations to foreign investors.

This alarming situation could lead England the way of Iceland – a sudden and harsh awakening to national insolvency.

Will Social Security be There For Us?

One of the biggest challenges facing the Obama administration is restoring the viability of the US Social Security system. We don’t know exactly when it will hit, but for years there have been whispers of an impending Social Security crash. As the baby boomer generation hits retirement, they may strain the system beyond its breaking point. Obviously a weak economy in which the younger generation has trouble earning cannot help this situation.

Americans are looking to Obama and his incoming cabinet to find a solution to this potentially disastrous issue. Should Americans be unable to receive Social Security, their faith in their govenrment will be seriously weakened, and consequences will run far deeper than the immediate problem of supporting the elderly.

Some Retailers Benefit from Crisis

While most retailers find their profits shrinking, there have been some big winners this holiday season. Most notably, those retailers known to offer low prices and affordable value have found their market share growing, at the expense of luxury and elite vendors. Walmart, for instance, reported that it has seen an increas in its sale of flat screen TV’s, one of the most desired and expensive holiday gifts.

More shoppers are also turning to non-traditional venues such as Ebay and Craig’s List to find merchandise at recession prices. We may see a realignment in the retail space in which luxury brands, which had experienced growth for many years, may be dethroned by value brands in the coming period. We will need to wait and see whether manufacturers and retailers can stay solvent selling goods at the razor-thin profit margins such venues provide.

What Will Santa Bring Shareholders?

Traditionally, we expect an end-of-the-year spike in stock prices. Investors are people too, and they are impacted by the optimistic holiday spirit. We also know that many people allocate their investment capital on a yearly basis and make investments around the new year.

This year, though, it’s hard to know what will happen. Prices seem quite depressed, making a spike even more likely, but at the same time the atmosphere of uncertainty may override the usual holiday cheer, encouraging those who still have spare cash to hold it.

Interest Rates Fall, and the Dollar Follows

Everyone wants the Fed to take action to get the economy back on track, but now it’s starting to look like measures taken to help one area can do damage in another, complicating matters further.

This week the Fed slashed interest rates, a move intended to stimulate growth in the local economy. But the move also makes dollar denominated investments less attractive to foreigners, driving their money out of the country and forcing the dollar down against most other currencies.

Times are stormy now, and we may not see interest and exchange rates stable again for some while.

Green is the New Green

One of the variables underlying the current economic crisis is of course the price of oil. From airlines to SUV owners, to those who heat their homes with oil, everyone is feeling the wild fluctuations in this commodity. Although oil is down right now, all rational projections are that the price of a commodity with a limited supply and a growing global demand will rise over the next few years.

So how will businesses that rely on energy for transportation and manufacturing stay profitable? How can we sustain the globalized business style that has come to dominate almost every industry? The only answer is to go green. Once the province of mystics and die-hard naturalists with little regard for the financial bottom line, environmental concerns are finding increasing interest in the boardroom. At it’s core, enviromentalism is about reaping the maximum productivity from the minimum of resources, an orientation that an operations officer can easily relate to. As we move forward, we are likely to find substantive environmental improvements resulting from an increase in business and transportation efficiency.

Who is Too Big To Fail?

For the past few months, we have been hearing debates about whether Bear Stearns, AIG, Lehmann Brothers, Chrysler, Ford, and GM are “too big to fail”, the assumption being that, were they to fold, they would take America down with them.

The question is, how does an influx of taxpayer money prevent failing? Isn’t the root cause of the current failures to be found with management, both on the financial side as well as the business planning side? How will the new cash from Joe taxpayer be spent differently from all the other money that has already been blown?

The hard truth is, that no business is too big to fail, to the extent that taxpayers should bail them out. Once we take this approach, we have chosen the inefficient and beauracratic road of the USSR and other communist countries, where the government basically is a giant conglomerate of failing businesses, propped up by outlandish taxes.

America is too big to fail, and in order to keep it alive, it must be quarantined from any mismanaged business. Other businesses will always rise on the ruins of today’s bankrupcies, but if we shy away from confronting the consequences of our actions, we will just be inviting a catastrophic day of reckoning at a future date.

The Sun Belt Lures Northeastern Realty Refugees

“Realty Refugees” are people who face homelessness as a result of the fall of real estate prices. Many of these people have “underwater” mortgages, debts that exceed the current value of the house. It’s getting to the point where some will be forced to sell their houses for whatever they can, then look for a new home.

But even in this depressing situation, there is a lifeline. Many houses in the northeast are still worth far more than comparable properties in southern cities like Charlotte, Atlanta, Austin and Phoenix. Some realty refugees from the north may find they can maintain their standard of living, IF they are prepared to relocate.

For those who have just lost a job, this may ironically make the transition easier!